Pharmaceutical Packaging

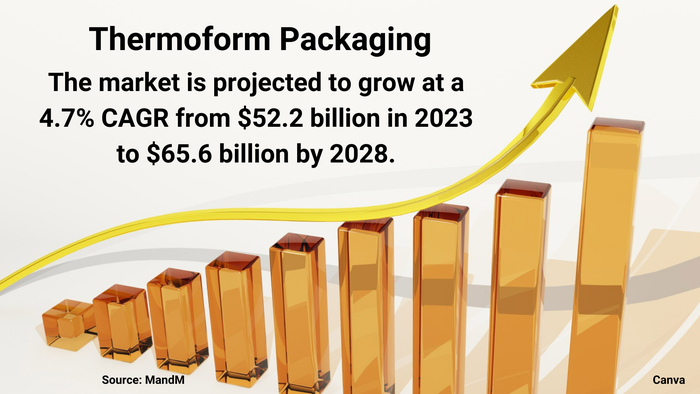

Thermoform packaging market graphic

Packaging DesignMarket Dynamics Favor Thermoform PackagingMarket Dynamics Favor Thermoform Packaging

Healthy demand from food and pharmaceutical companies will spur growth, despite sustainability challenges.

Editors' Choice

Sign up for the Packaging Digest News & Insights newsletter.